Fixing India’s Backbone

Solving India’s MSME Problem Has to Start with Fixing Data. Covid-19 May Provide a Lesson.

Covid-19 and the associated economic fallout has only reinvigorated an existent narrative on the financial vulnerability of MSMEs. The harsh structural forces at-play, such as MSMEs’ insufficient access to formal credit and an off-grid presence for the majority would continue to suppress their potential, with or without a pandemic or stimulus in the background.

That said, the current crisis does provide a unique opportunity to accelerate a much-needed reform agenda for the future. To make these reforms effective, the first step should be to target information asymmetry.

Missed the Boat

A lot has been said on how India’s Micro, Small & Medium Enterprises (MSMEs) form the country’s socio-economic backbone. In spite of being responsible for 37% of India’s gross domestic product (GDP), 40-45% of exports, employing 40% of our workforce i.e. c 110 million people, MSMEs in most cases have missed the boat when it comes to the nation’s gleaming post liberalisation narrative.

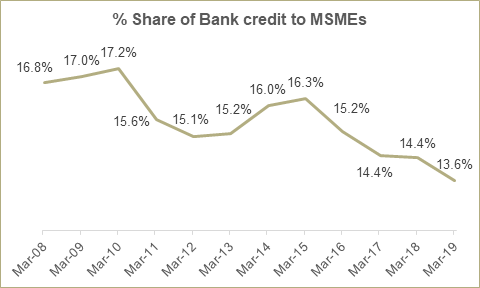

They remain highly fragmented, comprising over 63.4 million mostly unincorporated businesses, of which 99.5% are classified as “micro” setups i.e. a single man or woman working on their own. Running on thin margins and tight working capital cycles, even minor delays in payments have the propensity to wreak havoc on their operations. Barely one-third of MSMEs’ addressable lending requirement, which amounts to around INR12Lcr ($156 billion) – of INR36Lcr ($468 billion) in total – is served by formal banking system channels as per the International Finance Corporation (IFC). And the share of Scheduled Commercial Banks (SCBs) is going further down, as evident in the next chart (Source: DBIE, RBI).

Most of the aforementioned “gap” is filled by informal lenders, leading to high and inefficient cost of borrowing.

“Credit penetration is particularly low for the MSME sector where the ticket size is generally believed to be between one to ten million rupees. Even though more than 95 per cent of accounts with SCBs are having sanctioned credit limit less than one million each, the amount outstanding on these accounts is only 23 per cent of the total”, said Viral V. Acharya, Former Deputy Governor of the Reserve Bank of India (RBI) in a speech.

And ironically this is despite MSMEs’ credit quality being on average better than larger companies. As per TransUnion Cibil, a credit information company, loans with ticket size exceeding INR25cr ($3.3 million) are Non-Performing (NPA) to the degree of 17.5% and beyond, while smaller loans preferred by MSMEs comprise NPAs of 10% and below.

Information Asymmetry

The primary factor driving the said risk aversion towards MSME lending is information asymmetry. Data for most MSMEs is fragmented, opaque, and often missing, leading to limited underwriting for any creditor.

“Information asymmetry with the borrower is the major difficulty faced by any lender while granting a loan. Put simply, the borrower has more information about her own economic condition and risks than the lender. Credit information systems aim to reduce this asymmetry by enabling the lender to know the credit history with past lenders and the current indebtedness of the borrower. They improve efficiency of credit allocation, as the lender can use credit information systems to properly differentiate and appropriately price (interest rate) as well as alter terms (maturity, collateral, covenants, etc.) of the loan”, Viral V. Acharya added.

Leave aside any deep dive information on MSMEs’ credit history, even high-level sectoral figures on the number of enterprises, associated workforce, financial performance, sources and uses of funds, details of loans sanctioned, repayments, maturity profiles, collaterals etc. is not readily available in a consolidated, consistent, and timely manner. There are multiple data banks, ranging from the RBI to the MSME Ministry, to Udyog Aadhaar, and Goods and Services Tax Network (GSTN).

Clarity at the organizational, town, city, or district level, available by time-series is virtually unseen. It is indeed no wonder that most numbers thrown in the public domain by stakeholders when it comes to MSMEs appear anecdotal, non-comparable and inconsistent.

Even the government’ recently announced (and much welcome) credit line of INR3Lcr ($40 billion) for MSMEs, as part of its Covid-19 relief measures, would prove to be elusive for the most vulnerable enterprises, owing to this fundamental lack of reliable information.

A Known Unknown

MSMEs reduced access to formal credit is an often cited point, with everyone from the RBI to SIDBI, at various stages having preached to the choir. In fact, RBI’s proposal to create a Public Credit Registry (PCR) in 2018 is testament to its topicality.

The proposed PCR architecture (Source: Report of the High-Level Task Force on Public Credit Registry for India, 2018) comprises a consolidated repository of “core credit information” which could be then tapped by various stakeholders i.e. borrowers, creditors, regulators, rating agencies etc., through the creation of a centralized data infrastructure. A secondary layer comprising business level details such as identification, financials, and fraud record were planned to be overlaid in order to map helpful identifiers.

While the scope and ambition of this project are admirable, its progress has transpired at a glacial pace. It was only in March 2020, two years after announcing, when Tata Consultancy Services (TCS) and Dun & Bradstreet were shortlisted as L1 bidders for operationalization.

Such slow pacing has an obvious reason. The government’s consistent preference to create a single-window, overtly centralized and if one may add, closed technology infrastructure, needs considerable resources and operational bandwidth. This, coupled with stringent SOPs would ensure such a project would not be possible without an army of technologists and expensive consultants, leave alone thousands of man-hours for platform development.

Enter Covid-19

It is certain that most of you at this moment would be able to track the number of confirmed cases, active cases, deaths, and recoveries of Coronavirus patients at a state, district, and/or city level anywhere in the country - in real time – on private platforms such as COVID19INDIA.ORG, Wikipedia, or Worldometer. Also available are rich visualisations, showing everything from growth rates, logarithmic charts, demographics, to details on essential supply providers mapped by geolocation.

Think about it. Non-official and private initiatives, where data is validated by a group of volunteers and published on a publicly available Application Programming Interface (API), such as https://api.covid19india.org/.

Many of these initiatives are using consumer-oriented cloud products such as Google Sheets to input and validate data sets from multiple public sources, be it Ministry of Health and Family Welfare (MoHFW), official Twitter handles, PBI, Press Trust of India, ANI reports etc. before verifying and publishing them through an API. Similar tools have propped up globally in record time for the wider public need, without state intervention, on a voluntary basis, and at not a significant cost.

They have shown that it is indeed possible to agglomerate and represent complex granular data at scale, using innovative, decentralized, even crowdsourced applications of technology. Without consultants, without L1 bids, and without regulatory control.

Why can’t we apply some of these principles (not all!) to solve the problem of poor quality MSME data?

The “MSME Tracker”

The MSME Tracker (or “Tracker”)is an envisaged open architecture platform, to collate and create user-friendly data visualisations of MSMEs in a timely, standardised, and like-for-like manner.

The Tracker should focus on impact of external intervention to or support for MSMEs, which is mostly transactional in nature: be it liquidity, bank funding, government subsidies, or tax breaks from various agencies, scheduled commercial banks (SCBs), NBFCs, and fintech platforms.

Such a Tracker would act as the first step in beginning to assess the impact and performance of the said interventions. Transparent representation of data would ensure that policy makers, the banking system, market commentators, media, and civil society can regularly gauge progress, while organically placing checks and balances to ensure future accountability.

MSMEs can venture into the formalised banking system by leveraging this tool, granting more colour and insight to credit information companies, ratings agencies, and creditors for effective underwriting.

Where to Start?

MSMEs face several fundamentally unique challenges:

They are Off grid: Many are not registered and have zero credit history within formal channels

They are Capital starved and Asset Light: Most operate on tight cash cycles and need short-term unsecured funds

They have Low Operational Bandwidth: They have resistance against heavy compliance due to skilled manpower scarcity

They are Highly Fragmented: The delta between their extremes i.e. Micro vs. Medium, is extremely wide and needs to be revealed for enhancing nuance and context to any policy action

Any data solution worth its salt should be sensitive to these structural issues.

With that in mind, here are a few guidelines to develop the envisaged Tracker:

Focus only on pressing and relevant data: Transactional and alternative data is more critical i.e. borrowings & repayments with creditors, markers designating sources and uses of funds, tax-related, locational, e-commerce, mobile phone usage, digital payments etc., vs. consolidated financial data of businesses which requires broader compliance reform to be put in place first. Focus on information which is available rather than information which should be available.

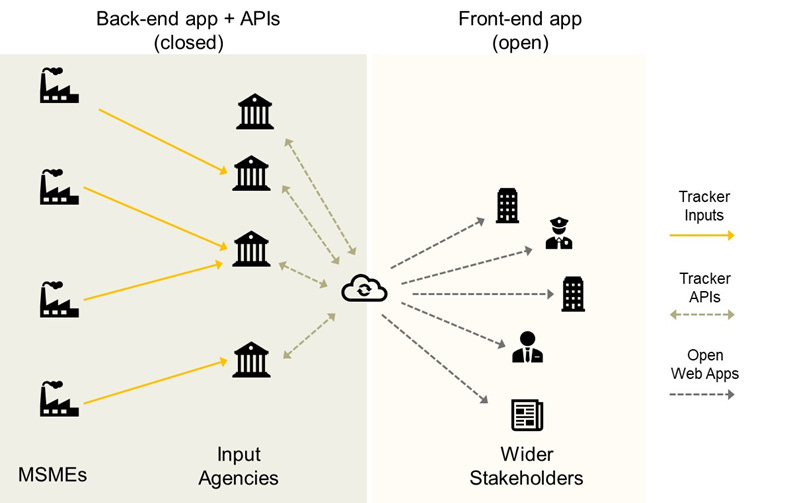

Tracker Input and Tracker APIs: Once the most relevant data metrics are locked, a back-end cloud-based application for onboarding MSMEs and collating inputs (“Tracker Input”) should be created. The architecture should be modular to ensure metrics and blocks can be added or amended at a later stage. Tracker APIs to fetch the inputs with relevant filters should be created.

Decentralised (or local) access of Tracker Input: Tracker Input should be made accessible to all regulated entities providing external interventions to or support for MSMEs (let us call them “Input Agencies”) i.e. branches of scheduled commercial banks, NBFCs, SIDBI, MSME Ministry, GSTN, Udyog Aadhar, Mudra Scheme, Udyami Mitra platform, government agencies, e-commerce platforms, fintech and payment platforms etc. These agencies would input data entries for every transaction. Data to be stored on cloud-based servers and be made accessible to all Input Agencies, irrespective of jurisdiction or location. MSMEs should though have final consent rights.

Variable access of Tracker APIs: All Input Agencies should have free access to Tracker APIs. Other stakeholders wishing to access APIs should be offered tiered pricing e.g. a free basic version and a paid advanced version. While the former would be available to individuals (policy makers, commentators, media), the latter would be available for enterprise use e.g. credit information companies and rating agencies. Resulting monetization should be used to fund storage and maintenance costs.

Use Covid-19 as an excuse to formalise: The pandemic should be used as an opportunity to onboard unregistered MSMEs using the promise of wage support as a bargaining chip. A recent survey of 5,000 MSMEs which do not provide essential services conducted by the All India Manufacturers’ Organisation (AIMO) found that 71% of said enterprises could not pay their worker salaries in the month of March. Wage support is the most direct and impactful way of helping them. The eligibility criteria for availing wage support should be one-time registration and compliance on the system which can be done at any Input Agency. A unique identifier (like Udyog Aadhar) can be allotted.

Duplication checks: Cross-mapping against Udyog Aadhar Memorandum (UAM), Mudra Scheme, SIDBI, MSME Databank, and Goods and Services Tax Network (GSTN), where at present most of the registered entities are mapped should be done to ensure no duplication occurs.

Verification: Onus of verification of Input and/or Onboarding and/or Duplicity should be on the MSME proprietor - transaction settlement should be subject to verification via Aadhaar OTP. Evidence of duplicity should bring penalties.

Open Architecture Web Applications: The government or regulator should not get involved in the business of creating user-facing web applications for customised data visualisations. Once API access has been paid for, private contractors (i.e. IT services companies, stakeholders) should be free to create their own web-based applications, subject to their or their client’s use-case.

Decentralisation and transparency would ensure that there are no free-wheeling bouts of lip-service within the political spectrum, media and even civil society and accountability comes back when it comes to the woes of MSMEs.

This email is prepared by Arkvega Advisory (or “AA”), the Institutional Advisory practice of Arkvega Partners LLP (https://arkvega.com) – an independent New Delhi based advisory and investment management firm.

We are open to explore synergies with professionals, corporates, investors, and relevant service providers at-large, from the perspective of advisory partnership and lead origination. Feel free to reach us out at:

Nikhil Arora | nikhil@arkvega.com | @Nikhil26A

Sharath Toopran | sharath@arkvega.com | @SharathToopran